Why can’t an origin that produces great coffee get a break?

As part of a presentation to discuss the impact of the global coffee market, I wanted to apply what I had just observed on a recent trip to BurundiBurundi coffee bears resemblance to neighboring Rwanda, in both cup character, but also the culture surrounding coffee. Burundi is a small landlocked country at the crossroads of East... ...more. Luckily I had a good data source to filter my observations through, an analysis of the Burundi coffee sector produced by a trio of economists and coffee market specialists.

The bigger question the case of Burundi raises for me as a coffee buyer, is this: “Why do we in the “specialty coffee” trade think we provide solutions to poverty and global inequality when, as in Burundi, farmers can produce great coffee and it doesn’t make an impact on their lives?” Yes, of course coffee buyers don’t think they have “the answer” and yet we market coffee in a way that pretends to be part of a global “solution”. Even with that, and allowing for personal and professional imperfection, my question is this: “Why don’t we at least try to understand the problems we observe in a greater context, including things not related to coffee?”

In other words, coffee is neither the cause nor the solution to systemic poverty and decreased life chances. How can we expand the discussion, and have those who engage in global issues by, perhaps, something as small as buying a coffee from a place like Burundi, look at a fuller picture of global trade and consumption?

Perhaps part of this also indicates a problem with the way coffee is marketed, in particular specialty coffeeSpecialty coffee was a term devised to mean higher levels of green coffee quality than average "industrial coffee" or "commercial coffee". At this point, the term is of... ...more, fair tradeFair trade is an organized social movement and market-based approach to empowering developing country producers and promoting sustainability.: Fair trade is an organized social movement and market-based approach... ...more, direct tradeA term used by coffee sellers to indicate that the coffee was purchased through a direct relationship with the farmer. Unlike Fair Trade and Organic certifications, Direct Trade... ...more and others where a social mission is wrapped into the consumer price. Perhaps in doing this we appease consumer conscience and absolve the consumer (and ourselves) or any responsibility to look further, to be curious and wonder what the effect of our consumption is? In that light, ethical consumption might breed complacency and ambivalence, not investigation and action.

Burundi Coffee Market and World Markets

The backdrop for this case study is the currently low arabicaArabica refers to Coffea Arabica, the taxonomic species name of the genus responsible for around 75% of the worlds commercial coffee crop.: Arabica refers to Coffea Arabica, the... ...more market, used as a price basis for financial trading in coffee futures contracts. It’s been well below $1.00, and recently was down at 80 cents. Most agree this is below the cost of production in all cases and in all places, whether a large operation or small holder farm.

But the impact is dramatic in Burundi in several ways. On the nation level, coffee represents the largest source of foreign currency coming into the country. A reserve of foreign currency is needed to maintain a good exchange rate with local currency, and to buy imports. Lack of foreign currency puts any small nations economy on a slide into inflation and further devaluation of the nations currency, which means further poverty.

From the CIA World Factbook (actually a great resource for basic data on nations and economies) here is a snapshot of Burundi in brief :

Burundi is a landlocked, resource-poor country with an underdeveloped manufacturing sector. Agriculture accounts for over 40% of GDP and employs more than 90% of the population. Burundi’s primary exports are coffee and tea, which account for more than half of foreign exchange earnings, but these earnings are subject to fluctuations in weather and international coffee and tea prices, Burundi is heavily dependent on aid from bilateral and multilateral donors, as well as foreign exchange earnings from participation in the African Union Mission to Somalia (AMISOM). Foreign aid represented 48% of Burundi’s national income in 2015, one of the highest percentages in Sub-Saharan Africa, but this figure decreased to 33.5% in 2016 due to political turmoil surrounding President Nkurunziza’s bid for a third term.

Burundi Coffee Potential and Problems

Burundi has fantastic quality potential in their coffee, but only a small portion is classified as “specialty coffee” and receives premiums above the global market price. But as important as undervalued price for the coffee from Burundi, is the decline in volume. The amount of coffee produced has been diminishing for the last 20 years, even as the government has takes steps to privatize the industry and attract investment.

On top of this, the older stock of coffee trees here, mostly traditional BourbonA coffee cultivar; a cross between Typica and Bourbon, originally grown in Brazil: Mundo Novo is a commercial coffee cultivar; a natural hybrid between "Sumatra" and Red Bourbon,... ...more varietyA botanical variety is a rank in the taxonomic hierarchy below the rank of species and subspecies and above the rank of form (form / variety / subspecies... ...more coffee, is subject to large biennial swings in the crop volume. A highly productive harvest is often followed by a disastrously low one. The impact is as severe as a low global market – even if the market price was very high per bag of coffee, what does it matter if you only have a few pounds to sell?

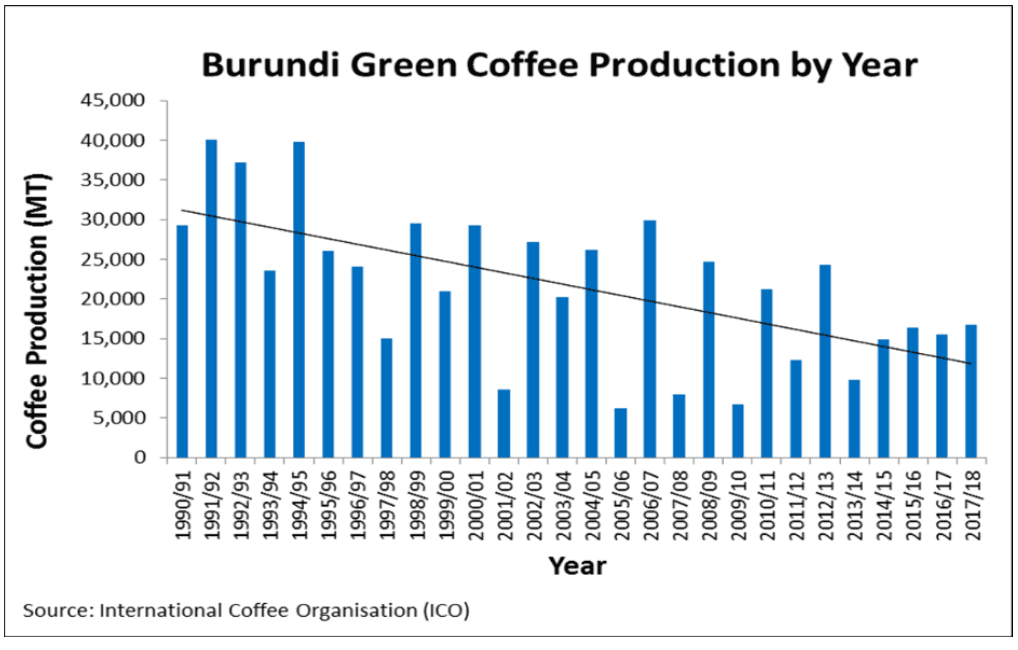

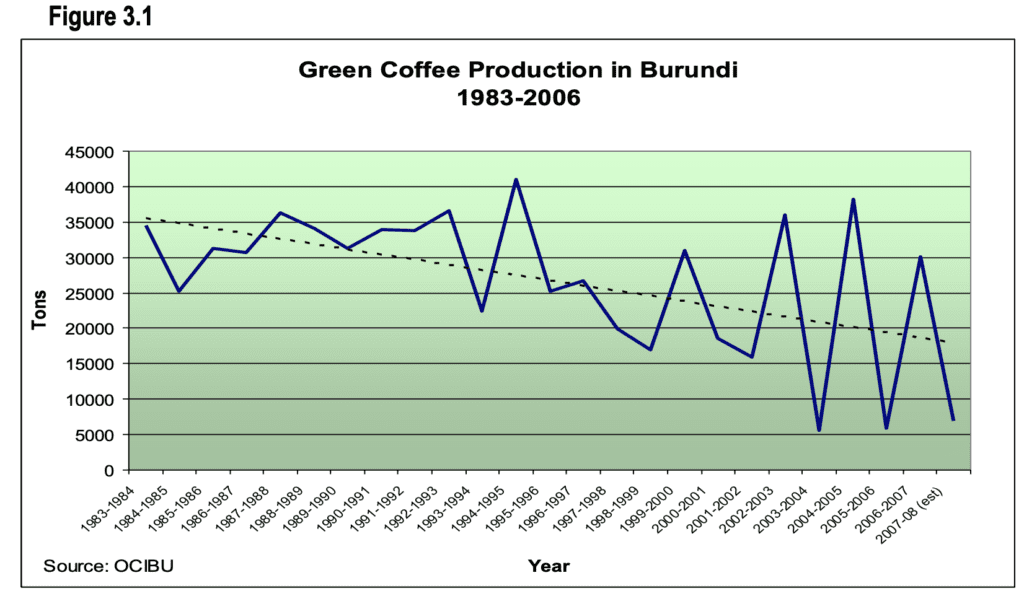

These charts, taken chiefly from USAID-funded analysis referenced below, and those by Dan Clay of Michigan State University say a lot about the issues of productivity of coffee and efficiency of labor on small coffee farms.

Big Swings in the coffee harvest total volume

Burundi coffee, like other origins with old trees, low levels of technical input and renovation of coffee, has huge swings in the total harvest volume. This can be due to other factors, weather cycles etc too. Here are two charts documenting crop cycle swings:

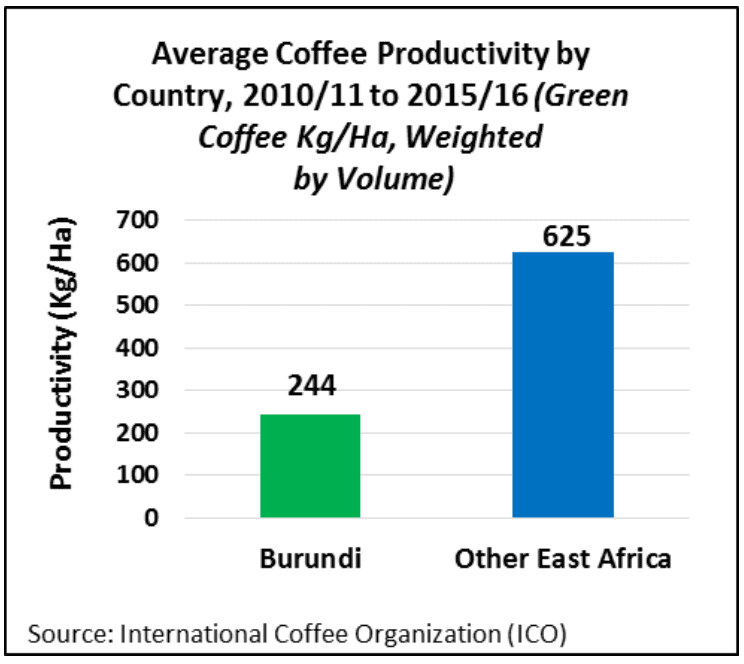

National productivity in coffee is low

Coffee farming in Burundi gets nowhere near the investment of most areas in East Africa, like KenyaKenya is the East African powerhouse of the coffee world. Both in the cup, and the way they run their trade, everything is topnotch.: Kenya is the East... ...more, where the price farmers get for their cherryEither a flavor in the coffee, or referring to the fruit of the coffee tree, which somewhat resembles a red cherry.: Either a flavor in the coffee, or... ...more is 4x that of Burundi. So it makes sense the investment and therefore productivity is low.

Filter this data through the the fact that 90% of the people of Burundi rely on agriculture for a cash crop (in addition to their sustenance food crops). And then consider how much of the countries income comes from coffee. As the value of coffee rises and falls, and the crop level rises and falls, this can create some years of abysmally low foreign currency coming into the country.

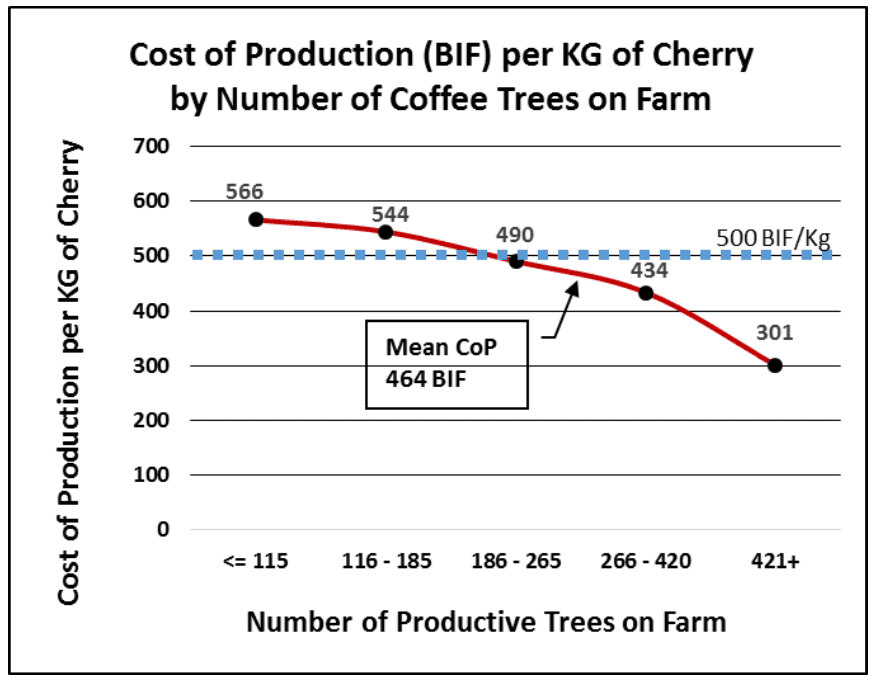

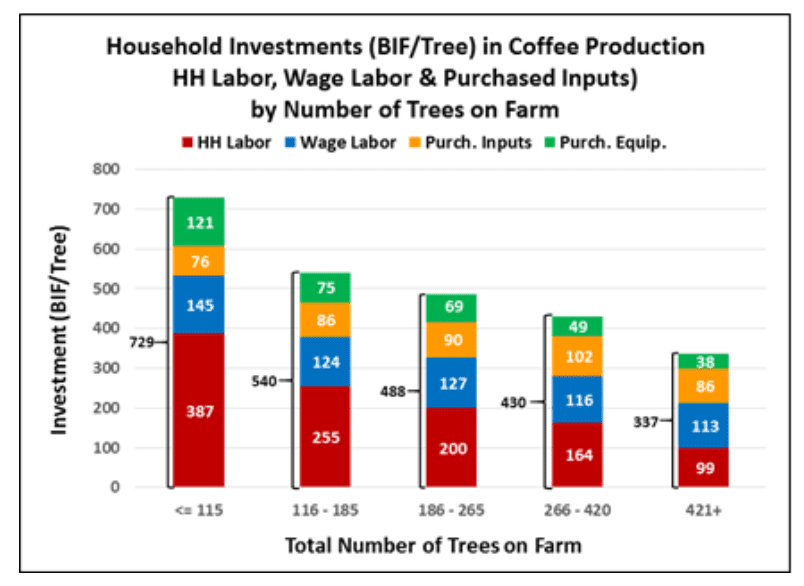

Relationship between size of farm and cost of coffee production

This was new information for me! There is a clear relationship between the benefit of coffee farming and the size of the farm (number of coffee trees) the farmer has. (BIF is Burundi Francs, the currency). So what you can see in the charts below is the smaller the farm, the worse the cost/benefit relationship. The second chart shows that the coffee investment takes more away from other family expenses with less trees.

From the charts, taken from Daniel Clay’s report on the Burundi coffee sector, we clearly see the lack of efficiency of the small coffee farm, the increased cost to produce coffee and the increase in the household income that must then go to the coffee farm, not to other family needs.

Coffee Can’t Fix All This, but…

I am not sure what the solution is, but the data is impelling. Some ideas are that small farmers might concentrate on a particular crop in their community, rather than have a little coffee, a little corn, a little vegetable etc. Or more cooperative pooled labor for coffee to make the investment more efficient. Coops that are well run offer many advantages to small farmers in this way, including the information sharing and technical training to increase yields. Another approach would be to coffee farmers lease their coffee farms to a particular person who focuses exclusively on coffee, and the leasee focuses on something else they can do with greater productivity. (I don’t just mean labor productivity here – I also mean replanting old unproductive trees etc) I really don’t know – this is not my expertise at all. But I observe and acknowledge the problems from first hand visits, and I acknowledge that there is a “bigger picture” issue in the agriculture sector in Burundi that doesn’t only have to do with coffee.

Of course, none of these approaches means much without going outside of agriculture. First there is the lack of political will, and presence of corruption and graft. That new “expert coffee farmer” I imagine above (perhaps naively) would need support from local programs, training, supplies that are bulk-purchased, new seedlings. That farmer needs health care for themselves and any laborers to they can work. They need a stable monetary system so their crop doesn’t lose value when converted to cash or credit. They need loans to finance the harvest. They need peace so they can work their farm without threat of violence, or being displaced from their homes or fields.

And they need a global market that doesn’t prey on them, to pit the value of their labor against every other laborer everywhere in the world.

– Thompson (article started 2018 and added thoughts August 2020)

Also see the article cited below and others on this page:

Coffee Science: Academic Papers and Documents

Full Text: Burundi Coffee Sector Diagnostic Study, Dan Clay MSU

Abstract:

The coffee sector in Burundi has reached a critical point in its development. Privatization and a certain amount of market liberalization have succeeded in attracting investment in coffee processingThe removal of the cherry and parchment from the coffee seed.: Coffee is either wet-processed (also called washed or wet-milled) or dry-processed (also called wild, natural or natural... ...more operations from both national and international sources. The number of washing stations has surged from 133 in 2008 to 267 ten years later. The number of dry mills has also more than doubled in the same time period—from four to nine. However, this growth in processing capacity has not been accompanied by a corresponding increase in coffee production. Rather, coffee production has been in structural decline for over 20 years and shows no sign of a rebound, despite the new investment flowing into the sector. This decline in production signals the persistence of a structural problem and threatens the viability of the sector as a whole, as lower volumes undermine the per unit profitability of processors and exporters. Since coffee provides around 80% of Burundi’s foreign exchange, declining production also contributes to current macro-economic difficulties posed by the scarcity of foreign exchange and the rapidly increasing differential between the cash and official bank exchange rates. Comparative analysis of Burundian farm gateFarm Gate Coffee is the name we give to our direct trade coffee buying program. Farm Gate pricing means that we have negotiated a price directly with the... ...more prices for coffee cherries vis-à-vis other East African countries, as well as survey responses from a sample of 1,024 farmers in Burundi’s primary coffee growing regionsCoffee is grown in a belt around the world - roughly from the Tropic of Cancer to the Tropic of Capricorn, and specialty coffee is grown generally from... ...more, suggest that a leading cause of the production decline is low cherry prices, which have eroded Burundian farmers’ incentives to invest in their coffee plantations. To reverse the decline, the GoB and the coffee sector actors together must develop a consistent strategy that will yield sustainable increases and stability in farm-level cherry prices. To make this happen, the coffee sector needs to adopt a common strategic framework for actors in the fully-washed market channel that prioritizes sales to the premium or specialty segments of the international coffee market. Selling to this segment of the market, which pays at least 10% above the NYBOT market price, is a realistic objective for all coffee washing stationIn Rwanda and some other East African countries, a wet mill is called a Washing Station.: In Rwanda and some other East African countries, a wet mill is... ...more operators in Burundi. Some Burundian coffee companies already sell at prices much higher than that. In order to facilitate this change, and to ensure that higher prices at the international market level flow down to farmers, a number of accompanying regulatory and policy measures will need to be taken by the GoB and the coffee sector regulator, ARFIC. These policy measures are: 1. Devaluing the Burundian franc. The current unusually wide gap between the cash and official bank foreign exchange rates serves to penalize all actors in the coffee sector by understating the value of coffee export sales in Burundian francs. This limits the ability of coffee washing stationIn Kenya, a "Factory" is actually a coffee wet mill (called a washing station in other parts of Africa) where the fresh cherry is brought for wet-processing. It... ...more operators to set attractive prices for cherries. A devaluation of a significant magnitude, possibly phased-in over time, would do much to resolve this problem. Failing an immediate devaluation, a temporary suspension of coffee sector payments for inputs through the input redevance and farmer contributions would help to relieve pressure on farmers from the overvalued franc. Another option on the table is that of a preferential exchange rate that would only apply to coffee exports. This may be a useful alternative as a short-term stopgap measure, but it would contribute to macro-economic imbalances if it persisted for any substantial length of time. 2. Fixing a stable multi-year minimum cherry price for farmers. Recent practices of setting minimum floor prices through negotiations among INTERCAFE partners have not resulted in prices that motivate farmers to invest more of their labor, cash and land in coffee production. To remedy this, the study team recommends moving to a three-year fixed minimum cherry price based on empirically derived cost of production data that would be set to ensure a predictable stable minimum price that is attractive to larger more efficient farmers—who have the most productive potential. The magnitude of the minimum price will be closely related to the magnitude of the devaluation; the larger the devaluation the higher the minimum cherry price. 3. Easing restrictions on the washed coffee channel. Actions taken since 2014 to periodically prohibit export and internal trading of washed parchmentGreen coffee still in its outer shell, before dry-milling, is called Parchment coffee (pergamino). In the wet process, coffee is peeled, fermented, washed and then ready for drying... ...more and exports of green washed coffee contribute to lower farmer incentives to invest in production. They also contribute to cross border flows that represent a drain on foreign exchange and create pressures for farmers to send lower quality cherries into the fully washed channel, which undermines the strategy for raising overall quality to reach the premium or above international market segments. These restrictions should be ceased and ARFIC/GoB should signal their long-term support for the washed coffee channel, while recognizing that washed coffee will diminish in importance as farmers are increasingly incentivized to produce for the higher-quality, fully washed coffee channel. 4. Easing restrictions on competition between coffee washing station operators in the market for cherries. Open competition among different coffee washing station operators has been shown by analysis to contribute to higher cherry prices for farmers. It also serves to create pressures for more efficient operation of washing stations. To facilitate free and open competition at this level, ARFIC should reverse recent regulations limiting the ability of coffee washing station operators to open secondary collection centers, as long as they meet the required technical and operational standards—essentially following the procedures that were in force in 2016. ARFIC should also reaffirm its intention to not modify the current regulations governing the placement of new washing stations, which prohibit new construction within 5 km of existing stations, but otherwise allow a large degree of freedom of implantation. 5. Eliminating restrictions on pre-campaign financing and terms of payment to farmers for cherries. Current regulations prohibit coffee washing station operators from contracting working capital loans with funders outside of Burundi. This was done to ensure transparencyTransparency is a flavor characterization synonymous with clarity. It is also a business ethics term, implying that as much information as possible about a product is made available... ...more in foreign exchange transactions so that ARFIC can be sure that actors respect requirements that all foreign exchange from coffee sales be repatriated. This measure limits washing station operators’ access to capital and limits their ability to compete with washed coffee buyers. By moving to a system of pre-approved foreign financing transactions with all foreign exchange in-flows being sent to the washing station operator’s mandated accounts at the BRB, ARFIC and the BRB should be able to have the degree of transparency required to track cash flows to determine whether coffee sales receipts have been repatriated. In addition, ARFIC should allow washing station operators to contract for payment of cherries with farmers as both parties deem desirable and possible—which should also foster increased competition that will favor farmers. 6. Restart the privatization process for remaining washing stations. The persistence of a dual system of public washing stations operating under management contracts along with pure private washing stations leads to doubts about the GoB’s commitment to market liberalization and creates competitive tensions due to differences in management models and cost structures. The GoB and its partners should press forward to execute the final round of privatizations, with a concerted effort to address the main institutional obstacle—which is the ability of farmer cooperatives to participate in the share offerings. This will necessitate a program of institutional support for cooperative strengthening and the adoption of clear guidelines for share purchase payments by the cooperatives. These guidelines would specify payment terms with schedules and default procedures that allow the reserved farmer shares to be offered to the majority owners or be rebid if the farmer cooperatives are unable to meet payment terms. In summary, sensible policy and regulatory changes starting with those described in this report will improve competitiveness and will incentivize farmers to invest more of their resources into coffee, bringing them on as full partners in value chain. These changes will help Burundi to reverse course and embark upon a virtuous circle that will benefit all actors at all levels. Farmer incentives result in higher yields and improved coffee quality. Higher volumes of quality, fully washed coffee will, in turn, yield lower per unit processing costs and more stable, better-paying buyers. Thus, higher prices will contribute to more generous margins across the board, enabling a renewed cycle of investments, including higher payments to farmers. This will place Burundi coffee on a steady path toward growth—a path that will drive a new wave of foreign exchange earnings and raise the country’s prospects for a sustainable future in coffee.

One Response

Thanks for waking me up and knocking me off my “seat of complacency”.

Good notes, and analysis.

I guess for now, keep buying from this region.